Product-led growth in 2026 is no longer an alternative go-to-market strategy — it is the default.Mixpanel’s 2026 State of Digital Analytics report, analysing behaviour across 12,000+ companies, named the product as the primary growth channel, with leading B2B SaaS companies now anchoring their growth strategy on in-product signals like feature adoption and time to value. Roughly 58% of B2B SaaS companies now run some form of product-led growth motion, and 91% plan to increase that investment over the next twelve months. Yet a quieter statistic undercuts the confidence: only 34% of PLG companies actively track activation — the single metric that best predicts whether a free user ever becomes a paying customer.

The gap between companies that understand product-led growth as a philosophy and companies that operate it as a measured, compounding system is where the real competitive advantage lives in 2026. This guide gives you the complete picture: what product-led growth actually means at this stage of the SaaS market, how the PLG motion has evolved under the pressure of agentic AI, which metrics actually predict commercial outcomes, and how to build the hybrid product-led sales architecture that the data consistently shows drives the strongest NRR.

What Product-Led Growth Means in 2026 — and How It Has Changed

Product-led growth is a go-to-market strategy where the product itself drives customer acquisition, activation, retention, and expansion. Instead of relying on outbound sales or marketing to push prospects through a funnel, PLG companies let users discover, try, and derive value from the product before they ever talk to a salesperson. The product creates demand. Sales captures and expands it.

The term was coined by Blake Bartlett at OpenView Venture Capital in 2016, but the underlying mechanics — freemium models, self-service onboarding, viral sharing loops — predate the label by a decade. Dropbox, Slack, Figma, and Calendly built their user bases almost entirely on PLG mechanics before the category had a name. What has changed in 2026 is not the fundamental economics but the sophistication of execution required to make PLG work at scale, and the structural shift introduced by agentic AI.

The critical evolution in product-led growth thinking for 2026 is the emergence of what practitioners are calling PLG 2.0 — the agentic PLG model where AI agents, not just human users, are the growth mechanism. Companies like Netlify report that 80% of their new signups are now AI agents rather than human users. The implication for product-led growth architecture is significant: the onboarding experience, the activation event, and the expansion trigger must be designed for both human and agent consumption simultaneously. PLG teams still running playbooks written in 2022 — built entirely around human self-serve activation — are seeing flat activation rates and struggling to diagnose why.

The Product-Led Growth Business Case: Why PLG Compounds in 2026

When auditing B2B SaaS architectures as a Digital Growth Specialist, my immediate focus is on whether the product-led growth motion is creating a closed loop between activation, product-qualified lead identification, sales conversion, and expansion — or whether PLG is functioning merely as a cheap acquisition channel without a commercial architecture around it.

The economic case for product-led growth in 2026 is based on three compounding advantages:

Advantage 1: Acquisition Cost Efficiency

Marketing and sales-led SaaS models scale revenue by scaling people. To double revenue under a traditional model, you often need to double the team — commissions, enablement, management overhead. Product-led growth breaks this dependency by shifting acquisition, user education, and demand qualification into the product itself, removing headcount as the primary bottleneck to growth.

The data validates the efficiency claim. Companies using Product Qualified Leads (PQLs) — users identified by in-product behaviour signals as ready for a commercial conversation — see 25% conversion rates compared to just 9% for marketing-qualified leads without product signals. That is a 177% improvement in conversion efficiency that directly reduces Customer Acquisition Cost (CAC) across the entire funnel.

Advantage 2: Faster Time to Value

Self-serve product-led growth companies demonstrate 18.3% higher scores on time-to-value delivery than companies without self-serve revenue. The forcing function is structural: if users must activate and find value independently, without a salesperson managing the process, the product must be genuinely intuitive and immediately valuable. Companies that pass this forcing function test build better products — products that retain users and expand revenue.

Advantage 3: NRR Compounding Through Expansion

The most powerful economic argument for product-led growth in 2026 is the NRR premium. Product-led growth companies with collaborative, team-based products systematically post higher Net Revenue Retention because the expansion mechanism is built into the product itself — additional seats, usage tiers, cross-product adoption — rather than depending on proactive sales outreach. Among companies above $50M ARR, PLG companies running hybrid models report NRR at 120%+ compared to 95–105% for comparable sales-led organisations.

The SaaS companies commanding the premium revenue multiples in 2026 — 8–12x ARR versus 3–5x for slower-growing peers — are predominantly PLG-first organisations with documented NRR above 110%. Product-led growth is not just a GTM efficiency play; it is a valuation architecture decision.

The Three Product-Led Growth Models: Freemium, Free Trial, and Hybrid

Choosing the right product-led growth entry model is one of the most consequential early decisions in PLG architecture. The three primary models have meaningfully different economics, and the data in 2026 is clear enough to make this a framework decision rather than a preference decision.

Freemium

Freemium offers a permanently free tier with limited functionality. Users can access the product indefinitely without payment, with upgrade triggers based on feature access, usage volume, seat count, or collaboration requirements.

Freemium achieves a 12% median visitor-to-signup rate — 140% higher than standard free trials — because removing the time pressure and payment friction generates significantly broader top-of-funnel volume. The conversion challenge is maintaining the quality of the pipeline. Freemium attracts a broader distribution of user intent, including users who have no commercial potential, which requires more sophisticated PQL qualification to identify the accounts worth investing sales resources in.

Freemium performs best for products where: value is genuinely demonstrable within the free tier without revealing the entire product, the product has strong viral or collaborative mechanics that drive organic network growth, and the upgrade trigger is naturally encountered during normal usage rather than arbitrarily imposed.

The notable trend in 2026 is the tightening of freemium tiers across major PLG companies. Slack, Notion, HubSpot, and Calendly have all reduced what is available for free over the past two years — a signal that the “give everything away and hope users convert” model has been stress-tested and found wanting at scale.

Free Trial

Free trial offers full or substantial product access for a defined period, typically 14–30 days, after which payment is required to continue. The time constraint creates urgency and focuses user activation efforts, producing higher activation rates than freemium for products that require meaningful setup before value is demonstrable.

Opt-in free trials — those that do not require credit card details at sign-up — achieve 17.8% conversion rates, making them the highest-performing entry model for products with moderate setup complexity and clear time-to-value within the trial window. The tradeoff is lower top-of-funnel volume compared to freemium, compensated by higher intent signals from users willing to invest time in setup without immediate payment.

Hybrid Product-Led Growth

The hybrid model — combining a free tier or trial with deliberate sales-assisted conversion for defined account segments — is the dominant architecture for product-led growth companies above $10M ARR. Approximately 67% of companies above $10M ARR run a hybrid PLG+SLG motion whether or not they formally label it as such.

The hybrid model works because product-led growth and sales-led growth address different purchase dynamics. Self-serve PLG captures the individual user, the SMB, and the product champion within a larger organisation. Sales-led expansion captures the enterprise contract, the multi-department rollout, and the strategic account relationship that a self-serve product cannot close alone. The companies that treat PLG and SLG as an either/or choice are leaving significant ARR on the table.

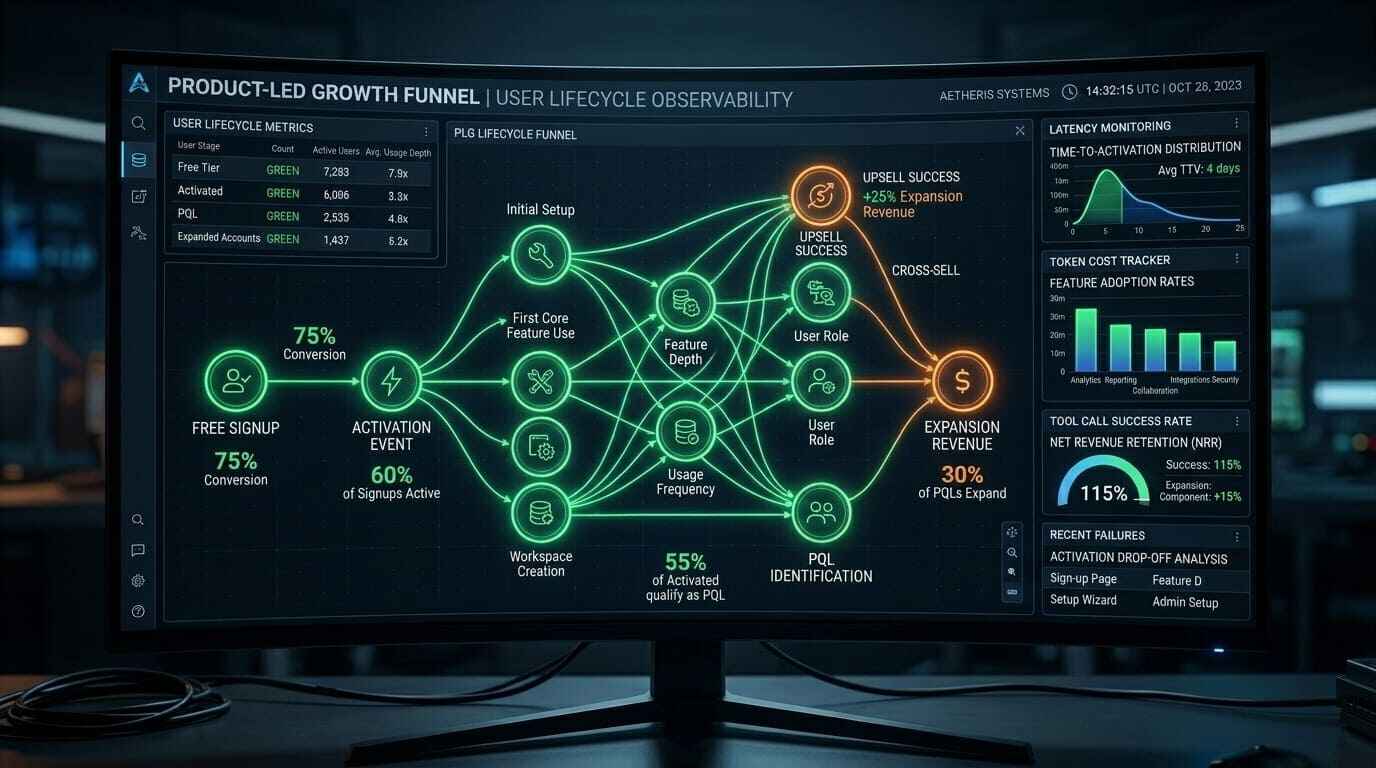

Product-Qualified Leads: The Core Commercial Architecture of Product-Led Growth

The PQL framework is where product-led growth converts from a product philosophy into a commercial system. Without PQL identification, product-led growth is just cheap acquisition with no reliable path to revenue. With a well-instrumented PQL framework, product-led growth becomes the most efficient commercial motion in B2B SaaS.

A Product Qualified Lead is a user or account that has demonstrated, through specific in-product behaviours, a readiness signal for a commercial conversation. The PQL definition varies by product and buyer profile, but the core architecture is consistent:

Step 1: Define the Activation Event. The activation event is the specific in-product action that correlates most strongly with long-term retention and payment. For Slack it was sending ten messages. For Dropbox it was storing at least one file. For a project management tool it might be creating a project and inviting a collaborator. The activation event is not the first login — it is the moment the user has experienced the product’s core value proposition.

Step 2: Identify the PQL Threshold. The PQL threshold is the combination of activation event completion, usage frequency, and account signals (company size, domain, behaviour patterns) that identifies users as commercially ready. Best-practice PQL frameworks combine product signals with firmographic data — a user who has hit the activation event at a company with 500+ employees and has invited three colleagues is a significantly more qualified commercial prospect than a solo user at a startup.

Step 3: Route PQLs to the Right Motion. High-value PQLs — enterprise accounts, multi-seat users, users who have hit upgrade triggers — route to sales for assisted conversion. Mid-market PQLs route to automated email sequences with targeted upgrade prompts. Self-serve PQLs are converted through in-product upgrade flows without human intervention.

Only 34% of product-led growth companies currently track activation — the metric most predictive of PQL conversion — despite 91% planning to increase PLG investment. The single highest-leverage improvement available to most PLG teams in 2026 is instrumentation of the activation event, not additional acquisition investment.

Product-Led Growth Metrics: The Complete 2026 Measurement Framework

In my 20 years of experience as a Finance Manager scaling technical infrastructure, the measurement failure I encounter most consistently in product-led growth organisations is the conflation of vanity acquisition metrics — signups, page visits, free trial starts — with the outcome metrics that actually predict revenue. A PLG motion generating 10,000 signups per month with 1% activation is not a growth engine. It is an expensive funnel with a broken middle.

The complete product-led growth measurement framework for 2026 includes:

Acquisition Metrics:

- Free tier signup rate: target 10–15% visitor-to-signup for freemium, 5–8% for free trial

- Signup-to-activation rate: target 40–60% within the first session for simple products, 25–40% for complex products requiring meaningful setup

- Organic versus paid PLG traffic split: best-in-class PLG companies drive 60–70% of signups from organic and viral channels

Activation Metrics:

- Time to activation event: target under 10 minutes for simple products, under 2 sessions for complex products

- Activation event completion rate: target 40%+ of signups reaching the defined activation event within 7 days

- D7 / D30 retention rate post-activation: target 60%+ D7, 40%+ D30 for strong PLG products

Conversion Metrics:

- Free-to-paid conversion rate: 2–5% for freemium (broad population), 15–25% for opt-in free trial (higher intent population)

- PQL-to-opportunity conversion rate: target 20–30% for sales-assisted PQL motion

- Time from PQL identification to sales conversation: target under 48 hours for high-value PQL routing

Expansion Metrics:

- NRR from PLG-originated cohorts: target 110%+ for team-based collaborative products

- Expansion ARR as a percentage of total new ARR: target 30–40% for mature PLG organisations

- Seat expansion rate per account at 90 days: the earliest and most reliable predictor of long-term NRR

Multi-Currency Benchmarks:

- Average PLG platform investment (analytics + onboarding + automation): $30,000–$80,000/year (USD) | £24,000–£63,000/year (GBP) | €28,000–€74,000/year (EUR)

- PQL routing and sales intelligence tooling: $15,000–$40,000/year (USD) | £12,000–£32,000/year (GBP) | €14,000–€37,000/year (EUR)

OpenView Partners Product-Led Growth resource

How Product-Led Growth Connects to the Broader SaaS Revenue Architecture

Product-led growth does not operate in isolation — it is the acquisition and activation layer of a broader revenue architecture that includes pricing strategy, customer success, and NRR management. The integration of these functions determines whether PLG compounds into a dominant competitive position or stalls at the $10M ARR ceiling that claims many PLG-first companies that have not evolved their commercial architecture.

The connection between PLG activation and pricing model is particularly critical in 2026. The shift from per-seat subscription pricing to consumption-based and hybrid pricing — a transition generating significant strategic debate across enterprise SaaS — directly affects PLG conversion mechanics. A usage-based pricing model creates natural PLG conversion triggers: as usage increases toward a tier threshold, the upgrade prompt is contextually relevant rather than arbitrary. This is why consumption-based pricing and product-led growth are increasingly deployed together as a combined architecture rather than as independent decisions.

For enterprise buyers evaluating SaaS vendors in 2026, the PLG motion also creates a new procurement dynamic: the product champion who activated through self-serve has already built internal advocacy before the formal procurement conversation begins. This bottom-up enterprise motion — where individual users or small teams adopt the product and drive upward budget allocation — requires a different approach to AI SaaS pricing strategy than traditional top-down enterprise sales, with pricing tiers designed to be commercially accessible at the individual level while scaling to enterprise contract values through usage, seats, or feature depth.

The NRR implications of product-led growth connect directly to SaaS net revenue retention benchmarks — PLG-originated customers who have experienced genuine product value before payment consistently outperform sales-led customers on 12-month retention, 24-month retention, and expansion rate. This retention premium is the compounding economic argument for PLG that goes beyond CAC efficiency.

The customer success dimension also matters. Agentic customer success functions that receive PLG-originated customers have a measurable advantage: product usage data collected during the free tier period provides a pre-activation health baseline that enables more precise onboarding and earlier identification of activation risk signals. This data inheritance from PLG motion to customer success motion is one of the most underutilised advantages in the SaaS architecture.

Building a Product-Led Growth Team: Roles, Structure, and 2026 Hiring Benchmarks

The product-led growth function in 2026 sits at the intersection of product, growth engineering, data, and commercial operations. The most common organisational failure in PLG is treating it as a marketing function (responsible for top-of-funnel volume) without the product and engineering ownership required to instrument activation, build upgrade flows, and create the in-product experience that converts users into paying customers.

The PLG team structure that supports $20M–$50M ARR typically includes:

- Head of Growth / VP of Product-Led Growth: Strategy ownership, PQL framework design, commercial integration with sales leadership

- Growth Product Manager: In-product activation flow ownership, upgrade experience, A/B testing programme

- Growth Engineer: Instrumentation, activation event tracking, PQL signal pipeline, integration between product analytics and CRM

- Data Analyst (PLG focus): Cohort analysis, conversion funnel reporting, activation rate modelling, NRR attribution by acquisition cohort

- Lifecycle Marketing Manager: Email and in-app messaging sequences for PLG conversion and expansion, working from PQL signals rather than time-based triggers

Compensation benchmarks for PLG-focused roles in 2026:

| Role | USA (USD) | UK (GBP) | EU (EUR) |

|---|---|---|---|

| Growth PM | $130,000–$175,000 | £100,000–£135,000 | €118,000–€160,000 |

| VP Product-Led Growth | $200,000–$280,000 | £155,000–£215,000 | €185,000–€260,000 |

| Growth Engineer | $140,000–$190,000 | £108,000–£147,000 | €128,000–€175,000 |

Strategic Outlook & Implementation

When auditing B2B SaaS architectures as a Digital Growth Specialist, my immediate focus in 2026 is whether the product-led growth motion creates a genuine closed loop — from activation event to PQL identification to commercial conversion to NRR-positive retention and expansion — or whether it remains a disconnected set of acquisition tactics without a commercial architecture around them. The gap between these two states is where most of the underperformance in PLG motions lives, and it is almost always a measurement and routing problem rather than a product or acquisition problem.

My implementation recommendation for SaaS founders running PLG in 2026 is to instrument activation before investing in acquisition. The 34% of PLG companies that currently track activation are operating with a systematic advantage over the 66% that are not — they know which acquisition channels produce activated users, which onboarding sequences drive the activation event, and which account profiles convert from activation to payment at acceptable rates. Without this instrumentation, increasing PLG acquisition investment is equivalent to pouring water into a leaking bucket and measuring the water added rather than the water retained.

The agentic AI dimension requires strategic attention that most PLG playbooks have not yet incorporated. If AI agents are evaluating SaaS products by the quality of their API, their MCP compatibility, and the ease with which automated workflows can extract value — rather than by the quality of their human onboarding experience — then the product-led growth motion must be re-architected for agent consumption simultaneously with human consumption. The companies that build this dual-audience PLG architecture in 2026 will hold a structural advantage as the agentic SaaS adoption curve accelerates into 2027 and beyond.

For enterprise buyers evaluating SaaS vendors whose products offer PLG entry points, my consistent advice is to treat the free tier or trial as a genuine due diligence mechanism, not just a procurement shortcut. The product usage data generated during a self-serve evaluation period — activation patterns, feature adoption depth, collaboration signals — is the most reliable predictor of whether a vendor’s product will actually embed into your workflows at the depth required to justify an enterprise contract. PLG entry points are not discounted products; they are information-rich evaluation environments. Use them as such.

Frequently Asked Questions About Product-Led Growth in 2026

What is the difference between product-led growth and sales-led growth in 2026? Product-led growth uses the product itself as the primary mechanism for user acquisition, activation, and expansion — users find value independently before a sales conversation occurs. Sales-led growth relies on outbound and inbound sales motions to identify, qualify, and close prospects before they have experienced the product. In 2026, the distinction is increasingly academic: 67% of companies above $10M ARR run a hybrid motion combining product-led acquisition and sales-led expansion. The question is not which model to choose but how to design the hand-off between the product-led acquisition layer and the sales-assisted conversion and expansion layer.

What is a Product Qualified Lead (PQL) and how is it different from a Marketing Qualified Lead (MQL)? A PQL is a user identified as commercially ready based on specific in-product behaviour signals — activation event completion, usage frequency, seat expansion, team invitation — combined with firmographic data about the account. An MQL is identified based on marketing engagement signals — content downloads, webinar attendance, email opens — without evidence of product value realisation. PQLs convert at 25% versus 9% for MQLs without product signals, making PQL-based routing a materially more efficient commercial motion for PLG companies.

What activation rate should a PLG SaaS company target in 2026? The benchmark for activation event completion within 7 days of signup is 40%+ for best-performing PLG companies. D7 retention post-activation should target 60%+, and D30 retention should target 40%+. If your activation rate is below 25%, the problem is almost always in the onboarding experience — either the activation event is poorly defined, the path to it is unclear, or the time-to-value is too long for the self-serve context. Fixing activation before investing in additional acquisition is the highest-leverage PLG improvement available to most teams.

How does product-led growth affect NRR benchmarks? PLG-originated customer cohorts consistently outperform sales-led cohorts on NRR due to three factors: higher activation rates at the point of payment (users who paid have already experienced value), stronger product dependency (activation requires genuine workflow integration), and more organic expansion triggers (collaborative products drive natural seat growth without requiring proactive CSM outreach). Best-in-class PLG companies with collaborative products target NRR of 120%+ from PLG-originated cohorts, compared to 95–110% for comparable sales-led acquisition cohorts.

When should a PLG company add a sales team? The typical trigger for adding a sales layer to a PLG motion is the appearance of enterprise accounts — companies with 500+ employees — adopting the product through self-serve channels and growing to $10,000+ ARR without a commercial relationship. These accounts represent significant expansion potential that self-serve mechanics alone cannot capture. A dedicated sales team focused exclusively on PLG-originated enterprise accounts — using product usage data as the primary qualification signal — consistently outperforms both pure PLG and traditional outbound sales in terms of ACV, CAC payback period, and first-year NRR.

Conclusion

Product-led growth in 2026 is not a trend — it is the structural architecture of B2B SaaS that compounds. The companies winning the valuation game, commanding premium NRR multiples, and building customer bases that expand without proportional headcount growth are almost uniformly running PLG-first commercial architectures with deliberate sales-assisted expansion layers for enterprise accounts.

The playbook has never been clearer. Define your activation event. Instrument it. Build the PQL framework that routes activated users to the right commercial motion. Design the upgrade experience so that conversion from free to paid is the natural continuation of value already experienced. Layer sales onto the product-led foundation where account size and complexity justify it. Measure NRR by acquisition cohort so you know whether PLG-originated customers actually retain and expand at the rates your valuation thesis requires.

The companies that execute this architecture in 2026 — across human and agentic user bases simultaneously — are building something that traditional sales-led competitors cannot replicate quickly: a product that sells itself, retains by delivering value, and expands because the workflow dependency compounds with every feature adopted. That is not just a go-to-market advantage. That is the most durable competitive moat available to a B2B SaaS business in 2026.

About the Author

Hi, I’m Ghulam Fareed. Over the last 10 years as a Manager and Digital Growth Specialist, I’ve focused on scaling technical B2B SaaS properties and navigating complex architectures. My work sits at the intersection of enterprise finance, AI infrastructure strategy, and operational efficiency — helping organizations translate SaaS ambition into auditable, scalable, cost-effective outcomes. I write at SaaS Latest News to share frameworks that enterprise leaders can apply immediately, not just read and file away.