The vertical SaaS startups building in 2026 are not chasing the same mass-market playbook that defined the last decade. They are owning single industries — construction, legal, veterinary, dental, logistics — and compounding switching costs that horizontal competitors simply cannot replicate. If you are a founder, investor, or enterprise buyer trying to understand where B2B software value is being created right now, vertical SaaS startups are the answer that keeps coming up in every credible funding dataset.

This pillar guide covers everything: what defines a vertical SaaS startup in 2026, which niches are genuinely underserved, how funding rounds are structured, what the strongest go-to-market patterns look like, and how to evaluate whether a vertical SaaS play has the architecture to scale past $10M ARR. I have spent time auditing B2B SaaS architectures as a Digital Growth Specialist, and my immediate focus is always on whether a product’s verticalization creates durable revenue or just a temporarily defensible niche with a ceiling.

What Are Vertical SaaS Startups and Why Do They Dominate 2026?

Vertical SaaS startups build software designed exclusively for a single industry — rather than the horizontal approach of building tools anyone can use. A vertical SaaS product for dental practices handles scheduling, insurance claims, compliance, and patient communication in one platform. A horizontal CRM handles contacts. The difference in switching cost and customer lifetime value is enormous.

In 2026, the vertical SaaS market is valued at approximately $94.86 billion, with 60% of small businesses now relying on vertical SaaS platforms for daily operations. The compounding effect of industry-specific data, workflow automation, and regulatory compliance integration has made vertical SaaS startups the most defensible category in B2B software investment.

The structural reason vertical SaaS startups win in 2026 comes down to three dynamics:

Data moats. Vertical SaaS platforms accumulate industry-specific data — claims histories, project cost benchmarks, patient outcomes — that general-purpose tools cannot replicate. This data becomes the AI training foundation for features that competitors cannot easily ship.

Regulatory alignment. As regulatory complexity increases — from EU AI Act enforcement in June 2026 to sector-specific data residency requirements — vertical SaaS startups that build compliance into their core product become the only viable procurement option for regulated buyers.

Willingness to pay. Vertical SaaS buyers face existential operational problems. They pay for solutions, not features. Average Contract Value (ACV) in vertical SaaS routinely reaches $12,000–$40,000 annually for mid-market customers, compared to $3,000–$8,000 for comparable horizontal tools.

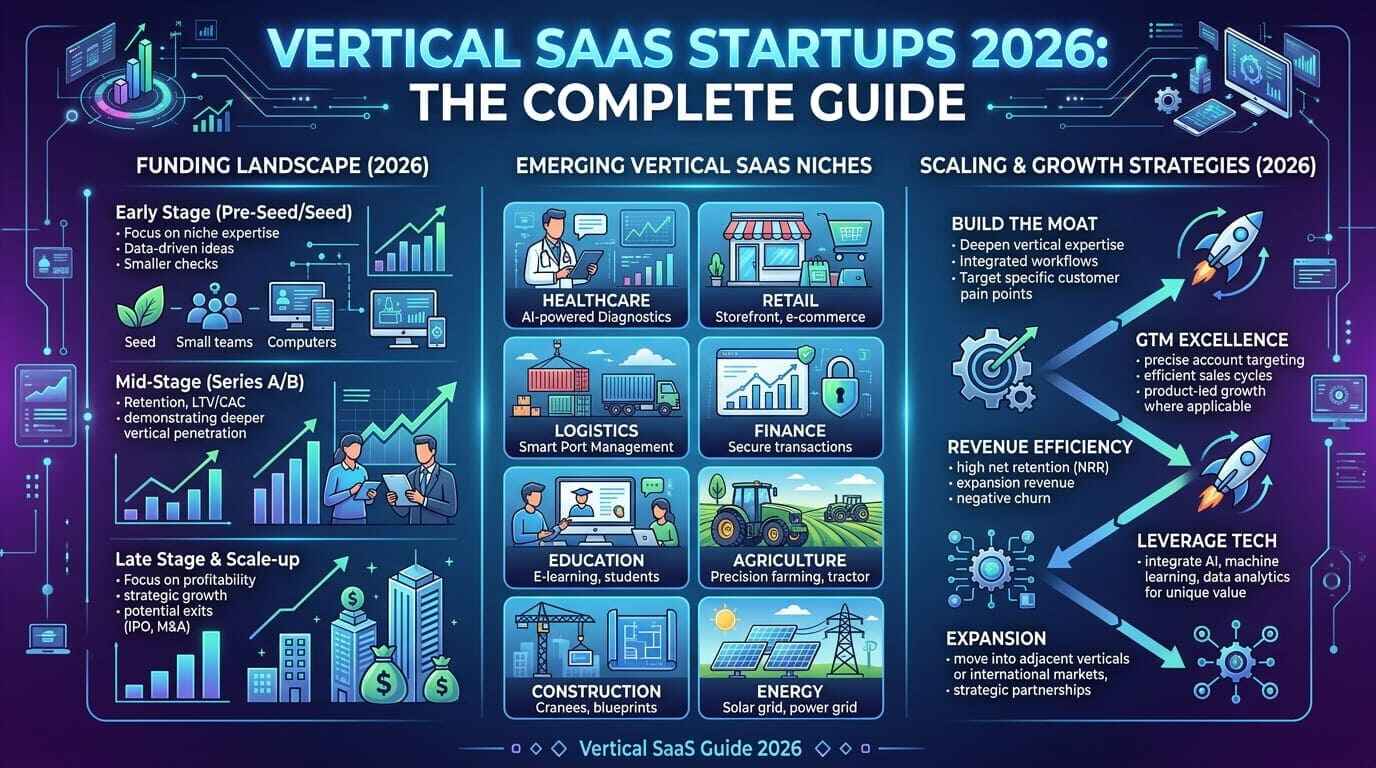

The Vertical SaaS Startup Funding Landscape in 2026

Understanding where capital is flowing into vertical SaaS startups requires looking past the headlines. Total SaaS funding has reached $187 billion in 2026 year-to-date, but the distribution has shifted dramatically toward focused vertical plays.

Seed Stage: The Bar Has Risen Significantly

The median post-money valuation for seed rounds hit $24 million in 2026, up from $18 million the previous year. Many vertical SaaS startups raising Series A have completed multiple seed extensions before reaching institutional VC metrics. Founders building vertical SaaS startups in 2026 should plan for a 24-month seed runway minimum if targeting Series A qualification without a bridge round.

Venture capital in 2026 is concentrating on specific verticals:

- Vertical AI platforms with industry-specific fine-tuned models

- Cybersecurity SaaS for sector-specific compliance frameworks

- Healthcare vertical SaaS with 28% projected year-on-year growth

- Construction and real estate SaaS driven by sustainability mandates

- Legal technology SaaS for contract intelligence and regulatory workflows

Series A and Beyond: What Investors Require

Revenue multiples have compressed significantly from the 2021 peak. Where vertical SaaS startups once commanded 20–30x ARR at Series B, 2026 benchmarks cluster around 8–12x ARR for companies with strong fundamentals. Growth above 40% year-on-year commands 7–10x revenue multiples; below 20% growth compresses to 3–5x.

Prominent investors backing vertical SaaS startups in 2026 include Bessemer Venture Partners, Accel, and Salesforce Ventures — all prioritizing platforms with measurable switching costs and documented Net Revenue Retention above 110%.

Landmark recent funding rounds illustrate the market confidence in vertical SaaS:

| Company | Vertical | Round | Significance |

|---|---|---|---|

| Procore | Construction | Growth | Workflow + compliance integration |

| Vetcove | Veterinary Supply | Series C | Procurement automation |

| Clio | Legal Management | Late Stage | AI contract workflows |

| Toast | Restaurant POS | Public | Vertical payments + analytics |

| Mindbody | Fitness & Wellness | Growth | Booking + retention platform |

The Highest-Opportunity Niches for Vertical SaaS Startups in 2026

When auditing B2B SaaS architectures as a Digital Growth Specialist, my immediate focus is on whether a niche has three characteristics simultaneously: unmet workflow complexity, a regulatory pressure accelerator, and low incumbent quality. In 2026, several verticals check all three boxes.

1. Construction SaaS for ESG Compliance

Construction is the dark horse vertical of 2026. The market for sustainability compliance SaaS in construction is estimated at $15 billion globally this year, driven by green building mandates across the EU and US. Vertical SaaS startups targeting mid-sized contractors need carbon footprint calculators, material sourcing audits, regulatory reporting dashboards, and BIM software integration.

The addressable buyer set is enormous and underserved: most compliance workflows still run on spreadsheets and consultancy retainers at $500 per hour. A vertical SaaS startup charging $200–$800 per month per project team and targeting $12,000–$40,000 MRR via B2B upsell cycles has a credible path to Series A in 24 months.

2. Healthcare and Dental Vertical SaaS

Healthcare vertical SaaS is tracking 28% projected year-on-year growth in 2026. The sub-niches with the highest low-competition opportunity are dental practice management, optometry workflow automation, and behavioral health billing. These buyers have high willingness to pay, strong switching costs once clinical workflows are embedded, and 65% average user stickiness scores.

AI-driven telemedicine platforms lead the healthcare vertical for non-technical founders entering regulated markets, with white-label infrastructure available from $100,000–$180,000 at launch.

3. Logistics and Last-Mile Delivery SaaS

E-commerce volume growth is creating structural demand for last-mile optimization tools targeting SMBs that cannot afford enterprise logistics platforms. Vertical SaaS startups serving regional logistics companies, delivery aggregators, and specialized freight operators can launch via white-label infrastructure from $80,000 and reach SMB customers at $300–$600 per month.

4. Legal Technology SaaS

Legal technology remains one of the most compelling verticals for SaaS startups. The EU AI Act enforcement timeline, which hit June 2026, created an immediate demand surge for AI risk assessment tools, algorithmic impact statements, and audit trail platforms. Companies deploying AI in Europe need compliance infrastructure that most are currently building with lawyers at $500 per hour. Vertical SaaS startups solving this problem are writing enterprise contracts at $50,000–$150,000 annually.

5. “Boring Industry” Vertical SaaS

The highest-signal niche pattern of 2026 is what analysts are calling “boring industry” vertical SaaS — HVAC management, pest control scheduling, roofing project management, and field service automation. These verticals show consistently low competition and high willingness to pay. Buyers in these industries have operational software needs as acute as enterprise CIOs, but have been ignored by mainstream SaaS vendors for years.

Vertical SaaS for boring industries consistently outperforms in Net Revenue Retention because there is no alternative to switch to.

Go-to-Market Architecture for Vertical SaaS Startups

The go-to-market failure mode for vertical SaaS startups is treating a niche industry like a horizontal market and investing in paid search too early. The core issue is structural: many vertical SaaS niches have fewer than 100 monthly searches for solution-related terms. Traditional SEO and paid search are inefficient at launch.

For vertical SaaS startups in 2026, the validated go-to-market architecture follows a three-phase model:

Phase 1 (Months 1–6): Outbound-Led Education

The first six months for a vertical SaaS startup should be dedicated entirely to outbound-driven pipeline building. The typical time to first revenue for mid-market SaaS ($10,000–$50,000 ACV) is 60–120 days. Outbound campaigns should educate the market on the problem — not pitch the product. Industry association events, direct LinkedIn sequences, and referral network activation are the primary channels.

This phase is about proving that buyers will talk, not just that they exist in data.

Phase 2 (Months 6–12): Inbound and Referral Activation

As initial customer success stories accumulate, inbound and referral traffic begins to compound. Case studies, compliance-focused content, and integration partner announcements drive awareness in industry-specific communities. SEO investment becomes viable once keyword clusters around the vertical problem space show 200+ monthly searches.

For vertical SaaS startups in the Startups category, building topical authority in niche industry media — trade journals, LinkedIn newsletters, association publications — outperforms general SaaS media exposure at this stage.

Phase 3 (Months 12–24): Product-Led Expansion

Vertical SaaS platforms that reach 50+ customers have enough workflow data to identify expansion triggers. Job changes among power users, project volume increases, new office openings — these are signals for automated expansion plays. Building PLG (product-led growth) loops into the platform creates a Net Revenue Retention flywheel that compounds toward the 110–120% NRR range institutional investors require.

Architecture Decisions That Define Vertical SaaS Startup Scalability

When auditing B2B SaaS architectures as a Digital Growth Specialist, my immediate focus is on whether the technical stack choices made at founding create or constrain scale. For vertical SaaS startups, three architecture decisions define whether the platform reaches $10M ARR or stalls at $2M.

Multi-Tenant vs. Single-Tenant Infrastructure

Most vertical SaaS startups launch on single-tenant infrastructure because regulated buyers in healthcare and legal often require data isolation. The cost is significant: single-tenant architectures require 3–4x more DevOps resources at scale. The optimal approach for vertical SaaS startups in 2026 is a hybrid multi-tenant core with isolated data storage per customer, using cloud-native solutions from AWS or Azure that separate compute from data residency.

This architecture supports enterprise sales cycles while keeping infrastructure costs manageable below $500K ARR.

AI Integration as Core, Not Feature

Vertical SaaS startups that treat AI as a feature — a “smart search” or “AI assistant” bolt-on — are building for commoditization. The 2026 market rewards vertical SaaS startups that integrate AI into the core workflow: predictive compliance alerts in construction SaaS, automated claims routing in healthcare SaaS, contract risk scoring in legal SaaS. Fine-tuned vertical AI models are now accessible at low cost, making proprietary workflow AI the strongest competitive moat available to vertical SaaS startups.

Integration Depth as Switching Cost Architecture

The most underappreciated architecture decision for vertical SaaS startups is integration depth. Every additional integration — ERP system, accounting platform, compliance database, industry-specific data source — increases the cost of switching for the buyer. Vertical SaaS startups that systematically build integration depth into their roadmap are building switching cost architecture, not just shipping features.

Celonis was initially dismissed as “too niche” by investors. Today it processes workflows for 99% of Fortune 500 companies. The pattern repeats: vertical SaaS startups that own one industry’s workflow data completely become generational companies.

How to Evaluate a Vertical SaaS Startup as an Investor or Acquirer

For investors and enterprise buyers evaluating vertical SaaS startups in 2026, the evaluation framework has shifted significantly from the 2021 hypergrowth era. Revenue multiples have compressed. Growth rate quality matters more than growth rate alone.

Net Revenue Retention above 110% is the primary signal that a vertical SaaS startup has product-market fit and is expanding within its customer base — not just replacing churn with new logos.

Customer Concentration Risk — no single customer representing more than 15% of ARR — indicates the platform has genuine market depth rather than a few anchor relationships.

Integration Ecosystem Breadth — measured by the number of active integrations customers use alongside the core platform — is the structural indicator of switching cost depth.

Vertical-Specific AI Adoption Rate — the percentage of customers actively using AI-driven features — signals whether the platform is genuinely verticalized or a horizontal tool with an industry-specific marketing veneer.

The most important due diligence question for a vertical SaaS startup is not “how large is the market?” It is: “what would it cost your customers to switch, and who would they switch to?” If the answer to the second part is “nobody,” you are looking at a generational business.

Vertical SaaS Startups vs. Horizontal SaaS: A 2026 Competitive Analysis

The tension between vertical and horizontal SaaS is not new, but the 2026 competitive dynamic has shifted decisively toward vertical platforms for several reasons.

Horizontal SaaS tools — CRMs, project management platforms, marketing automation — have reached feature saturation. Every buyer segment has adequate options. The competitive dynamic is on price and integrations, which is a commoditization race. Enterprise SaaS workflow automation tools that attempt to serve every vertical are increasingly losing deals to purpose-built vertical platforms that deliver faster time-to-value.

Vertical SaaS startups in 2026 win against horizontal incumbents on three consistent dimensions:

- Faster implementation: Industry-specific templates, pre-built compliance frameworks, and workflow defaults reduce implementation time by 60–70% compared to generic platforms requiring custom configuration.

- Higher user adoption: End users in specific industries recognize their own workflows in vertical SaaS. Adoption rates in construction SaaS and healthcare SaaS platforms consistently exceed 80%, compared to 40–60% for horizontal tools deployed in the same buyer segment.

- Lower support burden: Vertical SaaS platforms support users who understand the industry. Documentation, training materials, and support workflows can be built for one domain rather than a general audience — reducing support cost per seat by 30–50%.

The implication for AI-powered SaaS pricing strategy is significant: vertical SaaS platforms have structural justification for premium pricing that horizontal tools cannot match. A dental practice management platform can charge $800 per month and face no competitive pressure from a $25-per-seat project management tool.

Strategic Outlook & Implementation

When auditing B2B SaaS architectures as a Digital Growth Specialist, my immediate focus is on which vertical SaaS bets have the combination of timing, technical moat, and buyer urgency that creates a fundable business in the next 12 months.

I have identified four vertical SaaS startup plays that meet my 2026 threshold simultaneously across all three criteria:

EU AI Act Compliance SaaS is my highest-conviction near-term opportunity. The enforcement window is now. Companies deploying AI in Europe need solutions today, and most are doing the compliance work manually. A vertical SaaS startup here is selling into active pain with a hard regulatory deadline — the strongest possible demand signal.

Construction ESG and Carbon Compliance SaaS is my 12-month infrastructure bet. The $15 billion market size, the absence of dominant incumbents, and the increasing stringency of green building mandates in the UK, EU, and California make this the most structurally compelling new category in vertical SaaS. The white-label infrastructure costs are manageable and the buyer’s willingness to pay is not price-sensitive — it is deadline-sensitive.

Dental and Optometry SaaS is my defensibility play. Healthcare vertical SaaS at the sub-specialty level has the highest Net Revenue Retention I have seen in B2B software — routinely above 120% — because switching costs are clinical. Once a dental practice’s scheduling, billing, and insurance claims are running on a platform, switching is a clinical liability risk, not just an operational inconvenience.

Boring Industry SaaS — HVAC, pest control, roofing — is my contrarian early-stage recommendation. The competition is genuinely low. The buyers pay well. The switching costs are high. The only reason these markets are underserved is that they are not exciting to pitch at a TechCrunch demo day. That is not a market problem. That is a founder optics problem that creates a real opportunity.

The vertical SaaS startups that will command the highest exits in 2026–2028 are being built right now in industries that most Silicon Valley founders would not consider building in. That is exactly why I am watching them.

The Role of AI in Vertical SaaS Startup Differentiation

The shift from AI-as-feature to AI-as-core is the defining architectural inflection for vertical SaaS startups in 2026. AI-powered SaaS churn prediction models are a useful reference point: the most defensible AI features in vertical SaaS are not generic LLM wrappers but fine-tuned models trained on industry-specific workflow data that the platform itself generates.

For vertical SaaS startups, the AI differentiation framework operates on three levels:

Level 1 — Workflow AI: Automating repetitive industry-specific tasks. Claims processing in healthcare SaaS. Material compliance checks in construction SaaS. Document review in legal SaaS. This level delivers the immediate efficiency gains (40–70% reduction in manual task time) that justify premium pricing and accelerate procurement.

Level 2 — Predictive AI: Using accumulated workflow data to surface business intelligence that buyers cannot generate themselves. Predicting compliance risk windows in regulated industries. Forecasting project cost overruns in construction platforms. Identifying patient churn risk in healthcare SaaS. This level creates the data moat that prevents competitive entry.

Level 3 — Autonomous AI: Agentic AI systems that execute multi-step workflows without human intervention. This is the 2026–2027 frontier for vertical SaaS startups. The platforms that reach Level 3 AI integration in their vertical will define the next generation of enterprise software acquisition targets.

According to Gartner’s 2026 Enterprise Software Report, by 2027, more than 50% of enterprise software procurement decisions will factor vertical AI capability as a primary evaluation criterion, up from 18% in 2024. Vertical SaaS startups building AI-native architectures today are positioning for that procurement wave.

Pricing Models for Vertical SaaS Startups in 2026

Pricing strategy for vertical SaaS startups differs materially from horizontal SaaS because buyer value perception is anchored to operational outcomes, not feature sets.

The three dominant pricing models for vertical SaaS startups in 2026 are:

Per-Project or Per-Outcome Pricing: Construction SaaS, legal SaaS, and project-based healthcare platforms increasingly price per project or per case rather than per seat. This aligns vendor revenue with buyer value creation and reduces the friction of seat negotiation in enterprise deals.

Platform + Consumption Hybrid: Core platform fees combined with consumption-based pricing for AI-driven features. A dental SaaS platform charges $400/month for the base platform and $0.50 per AI-generated insurance claim. This model captures value from high-frequency workflow users while keeping the entry price accessible.

Outcome-Based SaaS: The most defensible pricing model for vertical SaaS. A construction compliance SaaS charges a percentage of avoided penalty liability. A healthcare SaaS charges based on revenue cycle improvement. Outcome-based pricing is difficult to implement at launch but commands 3–5x the revenue per customer of feature-based pricing.

In USD terms, vertical SaaS pricing in 2026 clusters around $200–$800/month for SMB buyers and $2,000–$8,000/month for mid-market enterprise. In GBP, equivalent benchmarks run £160–£640/month (SMB) and £1,600–£6,400/month (enterprise). EUR equivalents are €185–€740/month (SMB) and €1,850–€7,400/month (enterprise).

Conclusion

Vertical SaaS startups in 2026 represent the most structurally sound category in B2B software investment. The combination of industry-specific data moats, regulatory tailwinds, AI integration capability, and compressed horizontal SaaS competition has created a window for vertical SaaS founders, investors, and enterprise buyers to build and bet on category-defining platforms.

The niches with the clearest 2026 opportunity — EU AI Act compliance, construction ESG, dental and healthcare sub-specialties, and boring industry field service — share a common profile: underserved buyers with high willingness to pay, no dominant incumbent, and a regulatory or operational forcing function creating urgency today.

For founders, the imperative is clear: pick one industry, go deep, build the switching costs, and compound the data moat. The vertical SaaS startups that follow this playbook in 2026 will look like obvious successes by 2028. The ones watching from the sidelines waiting for a less competitive horizontal market to emerge will be watching a much longer time.

The vertical SaaS startups winning right now are not waiting for permission. Neither should you.

Frequently Asked Questions

Q1. What is a vertical SaaS startup and how does it differ from horizontal SaaS? A vertical SaaS startup builds software designed exclusively for a single industry — such as dental practice management, construction compliance, or legal contract intelligence. Unlike horizontal SaaS, which serves any buyer segment with general-purpose tools, vertical SaaS embeds industry-specific workflows, compliance requirements, and data models that create high switching costs and strong Net Revenue Retention.

Q2. Which vertical SaaS niches have the lowest competition in 2026? The lowest competition verticals in 2026 include “boring industry” field service (HVAC, pest control, roofing), construction ESG compliance, dental and optometry SaaS, and EU AI Act compliance tooling. These markets share high buyer willingness to pay with very few established software incumbents.

Q3. How much funding do vertical SaaS startups typically raise at seed stage in 2026? Seed stage valuations for vertical SaaS startups hit a median post-money of $24 million in 2026. Most startups completing seed rounds are planning for 24-month runways before reaching Series A qualification metrics, which typically require 40%+ year-on-year growth and NRR above 110%.

Q4. What revenue multiples do vertical SaaS startups command in 2026? In 2026, vertical SaaS startups with strong fundamentals (40%+ growth, NRR >110%) command 8–12x ARR at Series B. Companies growing above 40% year-on-year command 7–10x multiples, while below-20% growth compresses to 3–5x. These multiples represent a significant compression from the 2021 peak of 20–30x but reflect durable, sustainable valuations.

Q5. How should vertical SaaS startups structure their go-to-market strategy in the first year? Vertical SaaS startups should focus the first six months entirely on outbound-led education — not paid search or broad content marketing. Many vertical niches have fewer than 100 monthly searches for solution-related terms, making traditional demand generation inefficient early. Direct outreach, industry association events, and referral network activation are the highest-ROI channels in months one through six, with inbound and referral compounding beginning around month six to twelve.

About the Author

Hi, I’m Ghulam Fareed. Over the last 10 years as a Manager and Digital Growth Specialist, I’ve focused on scaling technical B2B SaaS properties and navigating complex architectures. My work sits at the intersection of enterprise finance, AI infrastructure strategy, and operational efficiency — helping organizations translate SaaS ambition into auditable, scalable, cost-effective outcomes. I write at SaaS Latest News to share frameworks that enterprise leaders can apply immediately, not just read and file away.